COSTS FOR BUYING A HOME

These are possible costs you may incur when you are purchasing your home…

In addition to the down payment on a home and mortgage loan amount, expect to spend approximately 3% to 4% of the home's purchase price on a variety of closing costs, such as property transfer tax, appraisal and survey fees, GST/PST, lawyer costs, etc.

Purchase offer deposit (Earnest Money Deposit)

Usually the deposit is paid when all conditions to the contract of purchase and sale are removed. But sometimes you may want to pay a small initial deposit when your offer is accepted. The deposit makes up part or all of your down payment. If you decide to back out of your offer without a justifiable reason, you'll lose the deposit.

- at least about 5%–10% of the purchase price

Down payment on a home

The minimum down payment you are required to pay is 5% of the home's purchase price. For your down payment, you can use gifts from others or, if you qualify as a first-time home buyer, some money from your RRSP account. Check for the latest updates from your Mortgage Specialist!

For first-time home buyers...

If you are a first-time home buyer, the Home Buyers' Plan (HBP) allows you to withdraw money for the down payment tax-free from your Registered Retirement Savings Plan (RRSP) account. Go to the government website for the lastest news.

How much can you withdraw?

- You can withdraw up to $25,000 from your RRSP.

- If you buy the home together with your spouse or partner, each of you can withdraw up to $25,000.

- Your contributions must remain in the RRSP for at least 90 days before you can withdraw them.

- You don't need to include this withdrawal in your income on your annual income tax return, and no tax is taken off the money you withdraw.

- Go to the government website for the lastest news.

What is the payback period?

- You don't have to start paying back to your RRSP until two years after you bought the home.

- You must pay back within 15 years by making RRSP deposits each year. CRA will determine your minimum yearly repayment amount and notify you once you need to start repaying.

- If you do not repay the amount due in a given year, it is included in your taxable income for that year.

- 5%–19.99% of purchase price for high-ratio mortgage

- 20% and up for conventional mortgage

- Go to the government website for the lastest news.

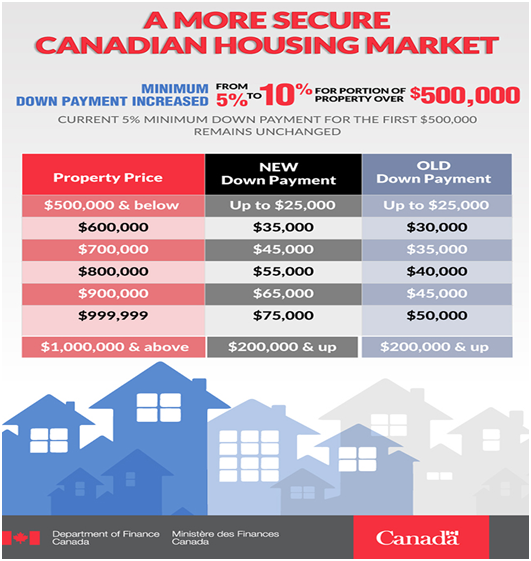

Down payment Changes for Purchases of homes AFTER February 15, 2016

- If you purchase a home UNDER $500,000.00 after February 15th, 2016, the rules don’t affect you

- If you purchase a home OVER $500,000, this could increase the amount of downpayment or deposit you need to make by approximately 1/3.

Example:

Instead of the current minimum down payment of 5% on the purchase price of the home, you will be paying 5% on the first $500,000 and 10% on the remaining portion over $500,000.

So if you bought a $750,000 home today, your minimum down payment would be calculated as 5% on the entire purchase price. 0.05 X $750,000 = $37,500 minimum down payment.

After February 15th, 2016 the minimum down payment would be calculated as 5% on the first $500,000 and 10% on the remaining $250,000. (0.05X $500,000) + (0.10 X $250,000) = $50,000 this is an increased upfront cost of $12,500 or 1/3 more savings required.

Source: Department of Finance Canada

Mortgage default insurance

If you've applied for a high-ratio mortgage, your lender will need mortgage loan insurance. This insurance helps protect lenders against mortgage default and is supplied by a third-party vendor like CMHC or Genworth Financial. Your lender may add the mortgage insurance premiums to your mortgage payments or ask you to pay it in full upon closing.

|

Premium scale for mortgage default insurance |

|

|

Down payment |

Premium on total loan |

|

5.00%–9.99% |

2.75% |

|

10.00%–14.99% |

2.00% |

|

15.00%–19.99% |

1.75% |

Mortgage application fee

Some lenders charge a loan application fee for processing your mortgage application. If your request for a mortgage is turned down, they normally return the fee. If you're using a mortgage broker, you may sometimes pay a mortgage broker fee (for example, if you have a poor credit history).

- $25–$100 for a conventional mortgage

- $75–$235 for a high-ratio mortgage

Home inspection fee

Although not required, a home inspection can find potential problems with the property and help you make an informed buying decision. Based on the inspection results, you may want to re-negotiate the purchase price or make the seller fix the problems out of his pocket.

- about $500 and up for a thorough inspection of a 2000 sq. ft.+ home

- $350 an up for a condo unit

Appraisal fee

Your mortgage lender may require an independent appraisal of the property to determine its market value. This value is established based on the property's present cash value, use, location, condition, the replacement value of improvements, net proceeds if the property is sold, and other factors. This is done to decide how much of a mortgage the lender will approve. If you have a substantial down payment, you can ask your lender to waive or absorb this fee. Some will, some won’t.

$250–$450 for most average properties

Property Transfer Tax

Property Transfer Tax (PTT) must be paid to the Province of British Columbia when your name is registered on the certificate of title with the Land Title Office. PPT is payable on the fair market value of the property, which is the same as the property's purchase price for a standard home sale transaction. For details, visit the B.C. Government's site.

You are charged property transfer tax when you make changes to a property's title, including:

- acquiring a registered interest in the property

- gaining an additional registered interest in the property becoming the registered holder of a lease, life estate, or right to purchase for the property

The amount of tax you pay is based on the fair market value of the land and improvements (e.g. buildings) on the date of registration unless you purchase a pre-sold strata unit. The tax is charged at a rate of:

- 1% on the first $200,000,

- 2% on the portion of the fair market value greater than $200,000 and up to and including $2,000,000, and

- 3% on the portion of the fair market value greater than $2,000,000, and

- If the property is residential, a further 2% on the portion of the fair market value greater than $3,000,000 (effective February 21, 2018).

For example, if the fair market value of a property is $450,000, the tax paid is $7,000.

Source:

https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax

http://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax/understand

For first-time home buyers...

If you are a first-time home buyer, you can be exempted from PTT if you meet all of the following requirements:To qualify for a full exemption, at the time the property is registered you must:

- be a Canadian citizen or permanent resident

- have lived in B.C. for 12 consecutive months immediately before the date you register the property or filed at least 2 income

- tax returns as a B.C. resident in the last 6 years

- have never owned an interest in a principal residence anywhere in the world at any time

- have never received a first time home buyers' exemption or refund

and the property must:

-

- be located in B.C.

- only be used as your principal residence

- have a fair market value of:

- $475,000 or less if registered on or before February 21, 2017, or

- $500,000 or less if registered on or after February 22, 2017

- be 0.5 hectares (1.24 acres) or smaller

You may qualify for a partial exemption from the tax if the property:

-

- has a fair market value less than:

- is larger than 0.5 hectares

- has another building on the property other than the principal residence

Find out the amount of your exemption if you qualify.

If you don’t qualify because you are not a Canadian citizen or permanent resident, but you become one within 12 months of when the property is registered, you may apply for a refund of the tax. To apply for a refund call (250) 387-0604.

Understand Your Taxes

You are charged property transfer tax when you make changes to a property's title, including:

- acquiring a registered interest in the property

- gaining an additional registered interest in the property

- becoming the registered holder of a lease, life estate, or right to purchase for the property

The amount of tax you pay is based on the fair market value of the land and improvements (e.g. buildings) on the date of registration unless you purchase a pre-sold strata unit.

The property transfer tax rate is:

- 1% on the first $200,000,

- 2% on the portion of the fair market value greater than $200,000 and up to and including $2,000,000,

- 3% on the portion of the fair market value greater than $2,000,000, and

- If the property is residential, a further 2% on the portion of the fair market value greater than $3,000,000 (effective February 21, 2018).

If the property is classified as residential and farm, or is residential mixed class (such as residential and commercial), you pay the further 2% tax on only the residential portion of the property.

For example, if the fair market value of a property is $450,000, the tax paid is $7,000.

Use this government online calculator to estimate you property transfer tax amount: https://forms.gov.bc.ca/taxes/estimate-your-property-transfer-taxes/

For further info on how to calculate (and source):

https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax

Pre-Sold Strata Unit

When you purchase a condo unit on the open market well in advance of the completion of the building, you will generally only pay tax on the total amount you paid to acquire the property. The total amount includes any money paid for:

- upgrades or additions,

- or any other premium for assignment of a written agreement

You may transfer the right to purchase the property to a related individual (doesn't include brothers and sisters) before the property is registered at the Land Title Office without affecting the taxable amount, but you may need approval from the developer.

New home purchases are also subject to 5% GST for the purchase.

If the right to purchase is transferred to someone that isn't a related individual, they will need to pay tax based on the fair market value of the property at the time the right was transferred.

This doesn't include bare land stratas.

Source: https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax/pre-sold-strata-unit

Survey fee

If you're buying a resale house (as opposed to a strata property or newly built house), your lending institution may request an updated property survey. Done by a registered land surveyor, a survey is simply a drawing of your property that confirms the lot size and shows the location of the house and other buildings. You and your lender need it to ensure that the buildings you’re buying are indeed within your property boundaries, that your neighbours' homes aren’t on your land, and that any buildings meet zoning regulations. An up-to-date survey is generally needed before you can legally be awarded title.

If the seller doesn't have a recent survey of their property, you can add a subject clause to your purchase offer making it the seller's responsibility to provide a Survey Certificate. Otherwise, you'll have to arrange and pay for it yourself.

About $1,000–$1,500 for an average property, depending on the property size

Goods and Services Tax (GST)

If you're buying a newly constructed or a substantially renovated (more than 90%) home, you will need to pay the Goods and Services Tax (GST) on the home purchase price. (British Columbia replaced the HST by the GST/PST on April 1, 2013.)

In addition to the GST, a buyer may also have to pay a transition tax of 2% if:

- the construction of the new home was at least 10% complete before April 1, 2013, and

- either ownership or possession of the new home transfers before April 1, 2015.

5% GST (plus 2% transition tax until April 1, 2015) on the home's purchase price

Legal costs

There are two types of legal costs:

- Fees — You will need a lawyer or notary public to handle the closing of the transaction. Fees are what you pay for the lawyer's or notary's time and expertise. Note that lawyer fees are not necessarily higher than notary fees.

- Disbursements — You will need to reimburse your lawyer or notary for any out-of-pocket expenses paid for documents and services provided by third parties. For a buyer, disbursement costs include such things as:

- various title search fees

- deed registration fee

- tax searches

- zoning searches

- faxes, phone calls

- courier costs and postage

- banking fees

- photocopying

fees: approximately $1000–$1,500 for common transactions with one mortgage (plus 5% GST). More complicated deals or more legal matters may increase the cost.

Title insurance

Title insurance, which is completely optional, protects a property owner against losses related to title defects. Most lenders will accept title insurance in lieu of a property survey. The coverage provided by title insurance companies typically includes:

- unknown title defects

- survey errors and errors in public records

- improvements made without the required building permits (unless made by you)

- existing liens against the property's title for unpaid debts by the previous owner (utilities, taxes, mortgages or condominium charges registered against the property)

- real estate fraud and forgery

- encroachment and unregistered easement issues

The insurance cost, which is a one-time premium with no deductible, depends on the type of coverage, the property's value, and the chosen provider

Contact your lawyer or notary for a quote.

Homeowner's insurance

Since your home will serve as the only security against your mortgage loan, you lender will require you to buy insurance in an amount equal to or greater than the mortgage loan. You must provide your lawyer with proof of insurance (called "Insurance Binder") by the completion date. Often insurance agents charge a fee of $25-35 for providing this Insurance Binder to your lawyer.

If you're buying a condominium, a strata corporation provides insurance for the overall structure and common areas of the building, as well as for the permanent features inside your unit, including kitchen cabinetry, flooring, built-in appliances, etc. Property insurance is included in your maintenance fees.

Cost varies widely, depending on your deductible, the value of your home and its contents, the type of coverage, and the insurer's rates

Adjustments costs

Adjustments are any costs prepaid by the seller that you'll have to reimburse when you take possession of the home. These costs may include property taxes, utilities, strata fees, and ongoing service contracts. On the completion day, you'll pay your portion of these costs in full.

Property tax adjustment — If the seller has already paid the full year’s property taxes to the municipality, you will have to reimburse him or her for your share of the taxes. Generally, property taxes are paid at the beginning of July for the full calendar year. If you purchase a property after July 1st, you will pay the seller the portion of the property tax for the days you own the property — from the completion day to December 31st.

Utility tax adjustment — In most municipalities, utility taxes (for water, gas, sewer, garbage, etc.) are also paid for the full calendar year. With metered services, the meters are read on the day the house changes hands to calculate the portions owed by the buyer and the seller.

Strata fee adjustments — If you are moving to a condominium, you'll be charged a monthly maintenance fee that covers the costs of common area maintenance and contributes to a contingency fund for future repairs. Since this fee is paid at the beginning of each month, the adjustment will be based on the number of days in your completion month that you have ownership.

Strata move-in fee

Many condominium complexes charge a fee when someone moves in or out of the building. This fee covers the installation of protecting padding in the elevator and the elevator key so that you can use the elevator exclusively during your move-in slot. You should reserve your move-in date with the strata management company as soon as possible.

Cost varies by strata, but commonly can be between $100–$300

Moving costs

Don't forget to budget for moving services and packing supplies. Shop around carefully before choosing movers and equipment. You can save about 50% by renting and driving a moving truck yourself.

$350 and up

Utility hook-up costs

Prior to the possession day you will need to contact utility companies such as telephone, cable, internet, hydro and gas to arrange for service. There may be fees associated with opening new service accounts and/or transferring existing ones.